Why Some Exchanges Block Withdrawals (and What It Means)

When a crypto exchange suddenly blocks withdrawals, it feels like the floor has dropped out from under you. This guide explains exactly why exchanges freeze withdrawals, how to tell the difference between routine risk controls and solvency problems, and what you should do in the first hour if it happens to you.

We’ll walk through how exchange custody actually works, the different patterns of withdrawal freezes, the role of reserve verification methods, what exchange “insurance” and SAFU funds really cover, and how to choose safer platforms in future. I’m drawing on more than a decade of hands-on experience with exchanges, internal risk systems, and incident tracking datasets that score platforms on security, transparency and withdrawal reliability.

If you want a broader checklist for evaluating platforms before you deposit, see the main Exchange Security Checklist, then come back here to understand what’s happening when things go wrong in real time.

At a glance: what a withdrawal block usually means

A withdrawal block is any situation where you cannot move funds off an exchange, even though your account shows a balance. That can happen at two levels:

- Account level: Only your account is affected (KYC issues, flagged activity, internal risk controls).

- Platform level: Many or all users are affected (maintenance, wallet issues, liquidity crunch, hacks, regulatory orders).

In practice, a withdrawal block is usually one of these:

- A temporary, controlled pause while the exchange upgrades systems or fixes a bug.

- A targeted freeze on specific accounts or regions for compliance reasons.

- A symptom of deeper trouble – a liquidity crunch or outright insolvency.

The same end result – “Withdrawals are temporarily disabled” – can mean anything from “we’re swapping a wallet server” to “we can’t pay everyone back”. Your job as a user is to quickly gather enough signals to decide whether to wait it out, cooperate with compliance, or start preparing evidence for a potential loss.

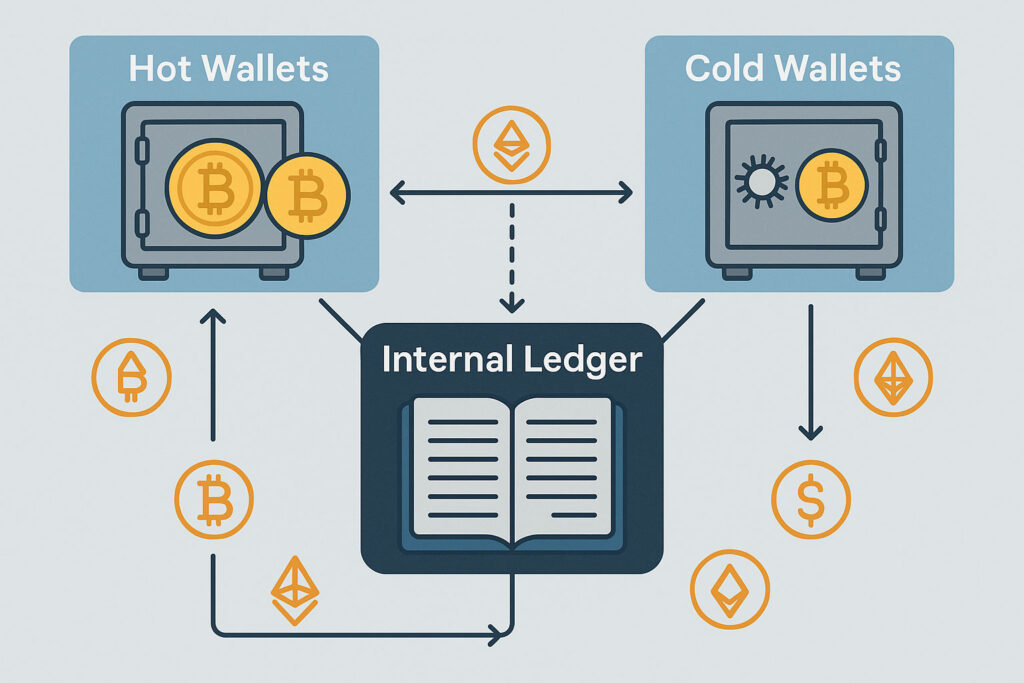

How exchange custody and liquidity really work

To understand withdrawal freezes, you first need a mental model of how an exchange actually holds your coins. It is not one address per user. In most centralised exchanges:

- User balances live in an internal database, not on-chain.

- Hot wallets hold a smaller operational float for day-to-day withdrawals.

- Cold wallets hold the bulk of customer assets, usually offline or under stricter controls.

When you deposit, the exchange credits your internal balance and eventually consolidates coins from deposit addresses into shared wallets. When you withdraw, the system:

- Checks your internal balance and risk profile.

- Queues a withdrawal request in a risk/AML system.

- Signs and broadcasts an on-chain transaction from a hot wallet (sometimes after a human or hardware security approval step).

From the outside, you only see the beginning (withdrawal requested) and the end (transaction hash, or a “failed” message). Everything in the middle is opaque, which is why freezes are so unsettling.

There are two broad failure modes:

- Operational failures: Systems, wallets, or risk engines are broken or overloaded, but the underlying assets exist.

- Solvency failures: The exchange doesn’t have enough liquid assets to honour all withdrawals, even if the software is working perfectly.

Most exchanges won’t clearly state which of these is happening. You need to infer it from behaviour.

Legitimate reasons exchanges may block withdrawals

Not every withdrawal block is a disaster. There are situations where a responsible exchange should pause withdrawals temporarily. The key is whether they communicate clearly, scope the issue narrowly, and restore service in a reasonable timeframe.

Compliance and AML flags

When an exchange detects patterns linked to money laundering, sanctions, or hacked funds, it may freeze individual accounts or specific withdrawals. This might be triggered by:

- Large, unusual withdrawals relative to your history.

- Links to flagged addresses or mixing services.

- Regulatory changes affecting your country.

In these cases, other users can still withdraw normally. You’ll typically be asked for more KYC documents, source-of-funds explanations, or to clarify the purpose of transactions.

Scheduled or emergency maintenance

Exchanges routinely upgrade wallet software, move funds between hot and cold storage, or patch security vulnerabilities. During that period they may:

- Pause withdrawals for specific coins (e.g. only BTC or only a certain chain).

- Pause withdrawals for a short window across the whole platform while they rebalance wallets.

Well-run platforms announce this in advance, give a time window, and stick to it. Poorly run platforms announce “maintenance” as a vague excuse for deeper issues.

Network congestion and fee issues

Sometimes the bottleneck is on-chain, not in the exchange. If network fees spike or blocks are full, exchanges may limit withdrawals to avoid users being stuck with underpriced transactions. Legitimate examples include:

- Temporarily raising minimum withdrawal amounts.

- Pausing withdrawals on a congested chain while they adjust fee calculations.

Again, these should be specific to a chain or token, not a blanket freeze on your entire account.

Security incidents caught early

In the best case, an exchange detects suspicious wallet behaviour early and pauses withdrawals while it investigates. You might see:

- A short, sharp freeze with frequent status updates.

- Public communication with clear timelines and technical details.

Here, a withdrawal block is a sign of a functioning security culture, not necessarily a failing one – as long as communication remains transparent.

Comparison table: typical legitimate pauses

| Scenario | Scope | Typical Duration | Red Flag Level |

|---|---|---|---|

| Scheduled maintenance | Specific coins or whole platform | Hours, maybe a day | Low, if announced and time-limited |

| KYC / AML review | Individual accounts | Days to weeks | Moderate, but usually account-specific |

| Network congestion | Specific chains | Hours to days | Low to moderate |

| Security patch with clear updates | Platform-wide or coin-specific | Hours | Moderate, trending lower with transparency |

Dangerous reasons withdrawals are blocked

Now for the uncomfortable part. The same “temporarily suspended” message can also signal a platform in real trouble.

Liquidity crunch or bank run

An exchange can be solvent on paper but illiquid in practice. For example, too much of its assets are locked in staking, lending, or long-term deals, while users suddenly demand cash or stablecoins. In this situation you may see:

- Slower and slower withdrawals before a full pause.

- Changing withdrawal limits without much explanation.

- Heavier use of obscure internal tokens or IOUs.

This resembles a bank run: first slower service, then queues, then a locked door. Once withdrawals are paused “for liquidity management”, the situation is serious.

Hidden leverage and insolvency

If an exchange has used customer deposits for leveraged bets, loans to affiliates, or risky yield schemes, it may simply not have the coins it claims. Common warning signs include:

- Overly generous rewards for holding or lending on the platform.

- Complex internal products that blur the line between exchange and hedge fund.

- Sudden changes to terms of service around ownership of assets.

When the market moves against them, these platforms can become insolvent almost overnight – and the first public sign is often a withdrawal freeze, followed by vague statements about “protecting users” while they search for a bailout.

Hacks and key compromise

Major security breaches can also trigger withdrawal blocks. If hot wallets are drained or keys are compromised, a responsible exchange must pause all outgoing transfers to prevent further loss. The difference between a robust and weak response is:

- Do they immediately disclose the incident and affected assets?

- Do they have a plan (and capital) to make users whole?

- Do they provide clear timelines and technical details once the immediate risk is contained?

An exchange that hides a hack for weeks, while quietly throttling withdrawals, is far more concerning than one that takes a reputational hit to protect users quickly.

Regulatory orders and legal freezes

Regulators, courts, or law enforcement can order exchanges to freeze assets, sometimes platform-wide, sometimes only for specific jurisdictions or users. In this case:

- The exchange may be legally limited in what it can say.

- Certain fiat rails (bank transfers, cards) may be affected more than crypto withdrawals.

- The situation may drag on while legal processes play out.

Again, consistent, factual communication matters. Silence and vague PR-language are red flags.

Rug pulls and outright fraud

At the extreme end are platforms that were never run as legitimate exchanges in the first place. Here, a withdrawal freeze is often accompanied by:

- Sudden disappearance of founders or executives.

- Channels closed or heavily censored.

- Websites going offline shortly afterward.

In these cases, recovery is usually limited to what regulators can claw back through long legal processes, often with low percentages returned to users.

Risk severity: how worried should you be?

| Scenario | Typical Messaging | Risk to Your Funds (★ = low, ★★★★★ = extreme) |

|---|---|---|

| Clear, time-boxed maintenance | Specific, with start/end times and progress updates | ★★☆☆☆ |

| Account-only KYC flag | Requests for documents, others can withdraw | ★★★☆☆ |

| Platform-wide “technical issues” with no detail | Vague, repeatedly extended deadlines | ★★★★☆ |

| Liquidity crunch / seeking “strategic options” | Talk of restructuring, investors, or “protecting users” | ★★★★★ |

Where proof of reserves fits in

One of the main tools users now look to is proof of reserves. At a high level, these are reserve verification methods designed to show that an exchange holds enough assets on-chain to match customer balances.

There are several models, each with trade-offs:

- Merkle-tree proofs: User balances are hashed into a Merkle tree, and the exchange publishes a root plus associated on-chain wallet balances. You can verify your own inclusion, but you must trust the liabilities side is complete.

- Third-party attestations: An auditor or specialist firm reviews wallet balances and internal records, then publishes a statement that assets exceed liabilities at a snapshot in time.

- Live on-chain feeds: For some exchanges and assets, you can see near-real-time wallet balances, sometimes with independent monitoring dashboards.

Each of these reserve verification approaches reduces information asymmetry, but none is perfect. Common pitfalls include:

- Only covering a subset of assets (e.g. BTC and ETH, but not smaller coins or liabilities such as loans).

- Relying on manual attestations that can miss off-balance-sheet risks.

- Publishing snapshots that do not guarantee ongoing solvency or liquidity.

A proof of reserves programme should be treated as one strong signal among many, not a guarantee that withdrawals will never be blocked.

Exchange “insurance” and SAFU-style funds

After several high-profile incidents, some platforms began marketing “insurance funds” or “SAFU” (Secure Asset Fund for Users) pools. These are designed to cover losses from hacks or other specified events – but the details matter.

When you see mentions of exchange insurance SAFU funds, you should ask:

- Is the fund segregated, transparently tracked, and independently auditable?

- What events are actually covered (hacks, internal fraud, insolvency, or only technical errors)?

- Is coverage per-user capped, or proportional to total losses?

- Are payouts discretionary, or governed by a formal policy?

Remember: these are not the same as government-backed deposit insurance. In many cases they are discretionary marketing features. Well-structured insurance and SAFU-style pools on exchanges can meaningfully reduce the impact of a hack, but they rarely protect users in a full-blown insolvency.

For a deeper breakdown of how these funds are structured, limits, and typical payout patterns, review the guide to insurance and SAFU-style funds on exchanges before assuming you are covered.

What to do immediately when withdrawals are blocked

The first hour after noticing a blocked withdrawal is crucial. You may not be able to move coins, but you can greatly improve your position if things get worse later.

Rapid response checklist

- Confirm the scope: Check whether the issue is only your account or platform-wide. Try a small withdrawal in a different asset; check social channels and status pages.

- Take screenshots: Capture your balances, recent transactions, and any error messages. Store copies offline as well.

- Export history: Download trade, deposit, and withdrawal histories in CSV or PDF if possible. Regulators or lawyers may need these later.

- Open a ticket: Create a support ticket describing the issue and keep a copy of the ticket ID and full text.

- Avoid adding more funds: Do not “average down” by sending more assets to a platform that may be in trouble.

- Document communication: Save emails, announcements, and status updates in a separate folder for future reference.

When the issue is account-specific

If others are withdrawing normally and your account is under review:

- Respond promptly to KYC/AML requests, but only through official channels.

- Provide clear, factual explanations of your source of funds.

- Do not fabricate documents or stories; that will make things worse.

This can be frustrating, but is often resolvable if your activity is legitimate and you have documentation.

When the issue is platform-wide

If status pages, social media, and third-party communities all report the same problem:

- Expect resolution to take longer; large-scale issues are usually complex.

- Follow official communication channels, not rumours.

- Consider how much of your total net worth is trapped and plan accordingly.

Your priority is to preserve evidence and avoid making the situation worse for yourself by panicking into risky behaviour.

When to walk away from an exchange for good

A temporary withdrawal issue is forgivable if handled well. Repeated issues, however, are a clear sign to leave. Strong indicators that it’s time to exit (once possible) include:

- Multiple “maintenance” windows with little technical detail.

- Frequent changes to withdrawal limits or fees without clear reasons.

- Opaque business structures, especially if assets are lent to affiliates.

- Executives or founders making contradictory or promotional statements during crises.

In my own practice, I treat any unexplained, platform-wide withdrawal problem as a one-time grace event. If it happens again without significantly better transparency, I plan to exit entirely as soon as withdrawals reopen and distribute funds across more robust venues and non-custodial wallets.

Choosing safer exchanges for the future

The best defence against withdrawal freezes is being picky about where you leave significant balances in the first place. A good starting point is to compare the top exchanges to choose instead, using criteria that go beyond fees and coin lists.

Key factors I look at include:

- Regulatory posture: Is the exchange licensed or registered in serious jurisdictions, with clear oversight?

- Custody model: Do they explain their hot/cold wallet architecture, key management, and separation of client assets?

- History of incidents: How have they handled past outages, hacks, or legal issues – swept under the rug or addressed transparently?

- Proof of reserves and reporting: Do they publish regular, meaningful transparency reports, not just marketing claims?

- Liquidity depth: Thin books are more vulnerable to market shocks; real liquidity is a safety feature, not just a trading one.

When using any of the stronger exchanges you can choose instead, I still operate on the assumption that “not your keys, not your coins” remains true. That leads directly to the next point.

Operational habits that reduce your exposure

Even on robust platforms, how you use exchanges matters as much as which one you pick. A few practical patterns dramatically reduce the harm a withdrawal freeze can do to you:

- Treat exchanges as transit hubs, not long-term vaults. Hold trading float there; move long-term holdings to non-custodial wallets.

- Spread counterparty risk across more than one venue. No single exchange should be able to freeze your entire crypto life.

- Maintain a fiat buffer outside crypto so you’re not forced to wait helplessly for a frozen platform when you need cash.

- Keep records updated: Regularly export statements in case you need them later for tax, legal, or recovery processes.

- Monitor status channels for the exchanges you use, so you’re not the last to hear about emerging issues.

These are the same habits used by professional desks and funds; retail users are often hit harder simply because they concentrate too much on a single platform and account.

Buying-guide style checklist: evaluating withdrawal risk

When you evaluate a platform, think like someone who has to live through a freeze tomorrow. Use this mini checklist:

- Before depositing:

- Read and understand the terms of service regarding ownership of assets and how they are held.

- Check whether the exchange publishes clear security and custody documentation.

- Look for meaningful transparency such as regular, independent reserve reports and clear governance over insurance funds.

- While using the exchange:

- Start with modest amounts and test deposits/withdrawals in both directions.

- Observe how fast withdrawals are processed under normal conditions.

- Monitor how the exchange communicates during minor incidents or maintenance.

- On an ongoing basis:

- Regularly rebalance to non-custodial wallets for long-term holdings.

- Keep no more than a predefined percentage of your net worth on any single platform.

- Review whether your chosen exchanges still meet your standards as regulation and market structure evolve.

Pros and cons of staying vs exiting after a freeze

| Option | Pros | Cons |

|---|---|---|

| Stay and wait for resolution | Avoid panic selling or rash moves. May benefit if the issue is genuinely short-term and well-managed. Less administrative overhead if service is fully restored. | Risk of sudden insolvency or extended legal processes. Opportunity cost if your capital is locked for a long time. Potential for deteriorating terms of withdrawal or haircut-style settlements. |

| Exit fully once withdrawals reopen | Eliminates ongoing counterparty risk from a platform that has shown weaknesses. Gives you the chance to reorganise custody to safer venues and self-custody. Sends a clear market signal that poor risk management has consequences. | Requires effort to reopen accounts elsewhere and update your workflows. May incur extra fees during periods of market volatility. You might lose access to specific products or markets only offered there. |

Why Some Exchanges Block Withdrawals FAQs

No. Short, clearly explained pauses for maintenance, wallet upgrades, or network congestion are normal in complex systems. The red flags are vague explanations, repeatedly extended timelines, and silence when things do not go according to the original plan.

Yes, exchanges can block withdrawals for a variety of reasons, including compliance checks, court orders, regulatory actions, security incidents, or operational issues. The legal context depends on where the exchange is based, how it is regulated, and what you agreed to in the terms of service.

At minimum, save screenshots of your balances, recent trades, deposits, and failed withdrawal attempts, plus copies of any support tickets and public announcements. If available, export CSV histories of your account activity. These records can be vital if there is later a recovery process, tax investigation, or legal action.

No. Proof of reserves can show that assets exist at a certain point in time, but it does not guarantee immediate liquidity, nor does it capture all off-balance-sheet liabilities. It is an important signal, especially when using robust reserve verification methods, but it should not be your only safeguard.

They can help, particularly in cases of limited technical hacks, but coverage is usually capped and can be discretionary. Many such funds do not cover insolvency or broad mismanagement. Always read how the fund is structured, funded, and governed before assuming you are protected.

There is no universal number, but a conservative approach is to keep only what you actively need for trading or short-term moves on exchanges, and hold long-term or strategic reserves in self-custody. The more concentrated your wealth is on a single platform, the more damage a withdrawal freeze can do.

Sending more money to the troubled platform in the hope of unlocking existing funds, or chasing rumours and unofficial “workarounds”. When withdrawals are blocked, assume the risk is higher than you can see and focus on preserving evidence and protecting your overall financial position.

Key takeaways

Withdrawal blocks are noisy signals: they can reflect responsible security practices or deep structural failures. Your job is to read the pattern:

- Is the issue narrow, clearly explained, and time-boxed – or vague and ever-extending?

- Are other users withdrawing successfully, or is the problem platform-wide?

- Does the exchange provide meaningful transparency, including robust reserves reporting and clearly structured insurance mechanisms?

Combine that situational awareness with conservative operational habits and careful choice of venues – leaning on curated lists of the top exchanges to choose instead – and a withdrawal freeze becomes an inconvenience, not a life-changing event.

Ultimately, the principle remains simple: any time you hand custody of your assets to an exchange, you gain convenience but assume counterparty risk. Understand how that risk manifests through withdrawal blocks, and you’ll be far better prepared when – not if – you see the “temporarily disabled” banner again.

If you found this content helpful,please consider sharing!:

More in Cryptocurrency